Deposit laddering: A smarter way to invest in GICs

If you’ve looked into investing in a Guaranteed Investment Certificate (GIC), you’ll know they’re a low-risk investment option that offers a guaranteed rate of return over a fixed period of time. GICs are a safe and reliable way to maximize your returns. Typically, to capitalize on the best rate, you need to lock your money in for a longer term — usually five years. But is it beneficial to lock in funds in today’s rising interest market?

Deposit laddering is an investment strategy that will help you maximize returns while offering the liquidity to tap into those funds on an annual basis. Instead of trying to time the market for the highest interest rate, with deposit laddering you can enjoy the benefit of a higher rate while still accessing part of your money each year.

The concept is simple—divide your total investment dollars by five and deposit these smaller amounts into each of the terms that SCU offers. As each term matures, lock it into a new term. This way, you will have a GIC that matures every year, giving you the option to access some of the money, re-invest what you have, or even add more funds to a maturing GIC.

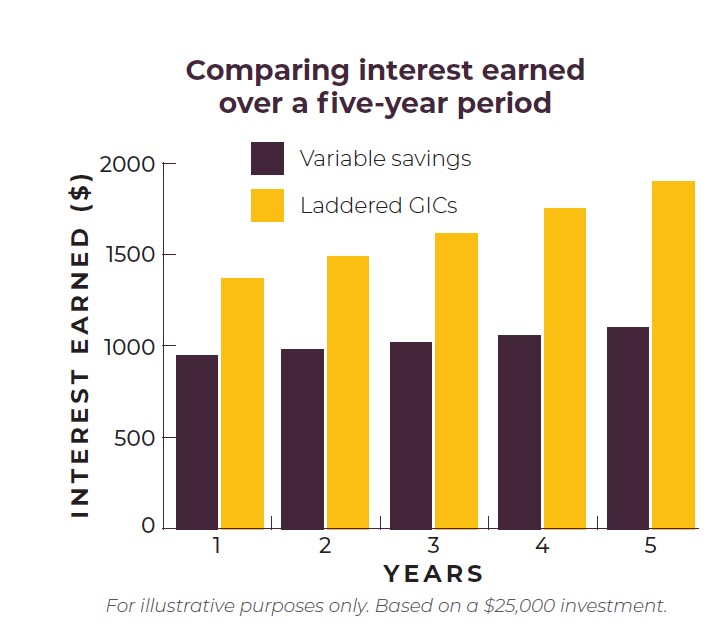

The graph below compares variable savings to a laddered GIC strategy, and illustrates the difference in interest earned over a 5-year period. The example uses interest rates at time of publication (November 2023) and an investment of $25,000. In this example, there is a 37% difference in return over the 5-year period. That’s because when you consider the actual interest earned year-over-year, the laddering strategy earns the average rate across all five terms.

You’ll earn more interest in the long run

With current interest rates, and assuming rates remain unchanged, there is an approximately 37% difference in return within five years between GIC laddering and investing the lump-sum in your variable savings. That’s because when you consider the actual interest earned year-over-year the laddering strategy earns the average rate across all five terms.

Money is still accessible when you need it

No one can predict the future. Your financial circumstances and savings goals will change over time, and you may need to access some of the funds in your GIC at some point. Deposit laddering keeps the ball in your court by giving you access to one fifth of your investments each year, without any penalties or costs. In addition, if you are living off the interest from your GIC portfolio, you can also structure cash flow to meet your specific needs.

You’re not as affected by the ups and downs of the market

Deposit ladders minimize the impact of rate fluctuations, but also allow you to stay current with market trends. Variable savings accounts will fluctuate, and even if you hold a single GIC, you’re limited to investing at whichever rate is offered when your investment matures. With deposit laddering, you don’t need to guess where interest rates are going. If rates go up, you will always have money coming due every year to take advantage of the rising rates. If rates go down, you benefit by having money invested for a higher rate in a longer term.

It’s a low-risk, secured investment

GICs are low risk because they offer a locked-in rate that is solely dependent on the length of term that you’ve chosen. In addition, at SCU, all deposits are guaranteed 100% by the Deposit Guarantee Corporation of Manitoba*.

If you’re looking for a low-risk investment strategy, deposit laddering is a great way to maximize your savings in a low interest market. We can help you build a savings strategy that works best for you. Call us at 1.800.728.6440 or fill out a contact form:

Contact us to discuss your next steps

*Includes all savings and chequing accounts, RRSPs, RRIFs,TFSAs, and GICs.

What is deposit laddering?

Deposit laddering is an investment strategy that will help you maximize returns while offering the liquidity to tap into those funds on an annual basis. Instead of trying to time the market for the highest interest rate, with deposit laddering you can enjoy the benefit of a higher rate while still accessing part of your money each year.The concept is simple—divide your total investment dollars by five and deposit these smaller amounts into each of the terms that SCU offers. As each term matures, lock it into a new term. This way, you will have a GIC that matures every year, giving you the option to access some of the money, re-invest what you have, or even add more funds to a maturing GIC.

The graph below compares variable savings to a laddered GIC strategy, and illustrates the difference in interest earned over a 5-year period. The example uses interest rates at time of publication (November 2023) and an investment of $25,000. In this example, there is a 37% difference in return over the 5-year period. That’s because when you consider the actual interest earned year-over-year, the laddering strategy earns the average rate across all five terms.

What are benefits of this strategy?

You’ll earn more interest in the long runWith current interest rates, and assuming rates remain unchanged, there is an approximately 37% difference in return within five years between GIC laddering and investing the lump-sum in your variable savings. That’s because when you consider the actual interest earned year-over-year the laddering strategy earns the average rate across all five terms.

Money is still accessible when you need it

No one can predict the future. Your financial circumstances and savings goals will change over time, and you may need to access some of the funds in your GIC at some point. Deposit laddering keeps the ball in your court by giving you access to one fifth of your investments each year, without any penalties or costs. In addition, if you are living off the interest from your GIC portfolio, you can also structure cash flow to meet your specific needs.

You’re not as affected by the ups and downs of the market

Deposit ladders minimize the impact of rate fluctuations, but also allow you to stay current with market trends. Variable savings accounts will fluctuate, and even if you hold a single GIC, you’re limited to investing at whichever rate is offered when your investment matures. With deposit laddering, you don’t need to guess where interest rates are going. If rates go up, you will always have money coming due every year to take advantage of the rising rates. If rates go down, you benefit by having money invested for a higher rate in a longer term.

It’s a low-risk, secured investment

GICs are low risk because they offer a locked-in rate that is solely dependent on the length of term that you’ve chosen. In addition, at SCU, all deposits are guaranteed 100% by the Deposit Guarantee Corporation of Manitoba*.

If you’re looking for a low-risk investment strategy, deposit laddering is a great way to maximize your savings in a low interest market. We can help you build a savings strategy that works best for you. Call us at 1.800.728.6440 or fill out a contact form:

Contact us to discuss your next steps

*Includes all savings and chequing accounts, RRSPs, RRIFs,TFSAs, and GICs.