GIC Explorer Guide

Jump to section:

1.0 The ABCs of GICs

2.0 Choosing the GIC that's right for you

3.0 Making the most of your GICs

4.0 Comparing GICs with other investment options

Prefer to download and read the full GIC Explorer Guide? Download the PDF

Feel free to skip to the sections that are most relevant to you. If you still have questions, or want some expert advice, we’re here to help. You can book an appointment, call us at 1.800.728.6440, or fill out a contact form to talk about your next steps.

1.0 The ABCs of GICs

GICs at-a-glance

There may be few guarantees in life; but fortunately for you, a GIC is one of them. A Guaranteed Investment Certificate (GIC) provides a guaranteed rate of return over a fixed period (although some GICs offer variable rates). With a GIC, your initial investment is protected, making GICs a safe and reliable way to grow your savings over time.

Translating GIC terms

As you consider a GIC, there are a few terms you need to understand to make the most of your investment.

- Principal investment: This is the initial amount of money you invest into your account. You’re guaranteed to receive your principal investment back, even with variable-rate or index-linked GICs.

- Interest rates: This is the rate of return you will earn on your investment. Some GICs offer tiered rates, meaning you will receive a higher interest rate the more you save. At SCU, our standard GICs come with tiered rates starting at $100,000*.

- Compound interest: Compound interest is key to understanding how your savings grow over time. Essentially, it’s the interest you make on your interest. For example, say you have a five-year GIC, and make $100 in interest at the end of the first year. You can cash it out and enjoy the rewards of your investment— maybe have a nice dinner. But if you skip the steak and keep that $100 in your GIC, you now have another $100 that’s earning interest in your account for the next year. This exponential growth can significantly increase your investment over time, even when interest rates are low.

- Term length: GICs lock in your investment for a set period of time, known as the term length. Term lengths can vary from months to years, depending on the product and financial institution.

- GIC maturity: This is the end of your GIC term. If you have a GIC at SCU, we’ll check in with you close to the maturity date to see what you’d like to do with your savings. You can choose to roll the funds into a new term (interest and all) or move your GIC funds to another account type.

Special terms related to Index-Linked GICs

Since Index-Linked GICs (ILGIC) are tied to stock-market performance, there are a few extra investment terms you’ll find helpful to know. More information the features and benefits of ILGICs can be found in sections 2.0 and 3.0 below.- Minimum performance guarantee: Some financial institutions will guarantee a minimum return on your investment (often a percentage), despite how the market performs.

- Maximum performance guarantee: Financial institutions will sometimes set a cap on your returns (often a percentage or set dollar amount), which limits your earning potential.

- Participation level: A financial institution may also limit your earning potential by setting a participation rate. This is a percentage based on market gains. For example, if you have a participation rate of 60%, your performance is only equal to 60% of the market returns.

Are GICs a safe investment?

One of the biggest appeals to GICs is in the name — they’re guaranteed. There’s no risk of losing your principal investment, and with fixed-rate GICs, you know your exact rate of return. Plus, at SCU, Deposits are guaranteed 100% by the Deposit Guarantee Corporation of Manitoba** (with the exception of the index-linked GIC where only the original investment is guaranteed). That said, there’s a bit more nuance to the questionthan you might think. There’s another factor to consider: rate risk. This is the risk you’re not earning enough on

your investments, especially when inflation is high. Locking in your money for a long period at a low rate during a time of high inflation could effectively mean your money loses value.

If you’re looking for advice on how to balance interest rates and inflation, call 1.800.728.6440 to contact a deposit specialist, fill out a a contact form , or book an appointment.

HOT TIP

Use the savings calculator for a quick and easy way to compare interest rates, term lengths, and principal investment to see how much more you can save.

The pros and cons of GICs

Are GICs a worthwhile investment for you? Before you decide, consider this list of pros and cons.

THE PROS- Guarantees your principal investment, including interest earned. (with the exception of Index-Linked GICs)

- Offers a higher rate than a variable savings account.

- Tiered rates allow you to earn even more interest the more you save.

- Having multiple term options means you can choose the term that aligns best with your savings goals.

- Available within an FHSA (First Home Savings Account), TFSA, RRSP, or RRIF to allow for tax efficiency. Explore all your options.

- Shields you from rate decreases.

- Typically requires no fees or additional charges to open.

- Prevents you from dipping into your savings by locking in your funds.

- Investment is usually non-redeemable before the end of the term (or if a GIC is redeemable, you may have to pay a penalty or get a lower rate to cash in early).

- Requires a minimum investment ($500 at SCU).

- You aren’t able to take advantage of rate increases. However, you can use investing strategies like deposit laddering to mitigate this risk.

- Typically requires your money to be locked in for several years at a time to receive the highest rates (with some exceptions).

- In times of high inflation, your long-term investments lose value if you lock in your funds at a low rate.

Opening a GIC

Considering opening a GIC? Here's how the process work at SCU.- Choose your term length: With a Standard GIC, you can choose a term that ranges from one to five years, and U.S. Dollar GICs are available in 30, 60, 90-day; or 1-year terms. Typically, with a GIC, the longer the term, the higher the interest rate (with some exceptions). Consider the longest term possible given market conditions and your timeframe for reaching your savings goal.

- Set your principal investment: At SCU, we require a minimum deposit of $500, but you may choose to deposit above this amount. Note that because GICs are a fixed product, if you have an additional amount you want to invest later, you will have to open a new GIC.

- Choose how to receive your GIC interest: You can choose to have your interest compound within the term or receive an annual interest payout to your account, as long as you choose a like-to-like transfer. For instance, each year you could have your TFSA GIC interest paid to your TFSA variable savings account.

- Decide where to deposit your funds upon maturity: When your GIC is about to mature, we’ll send you a reminder. You can choose to roll the funds into a new term (interest and all) or have the GIC funds set to be added to another savings vehicle of your choice.

- Because funds are not accessible until your GIC matures, it’s also wise to keep some cash savings readily available (within a High Interest Savings Account, for example) to help you manage the unexpected.

- We offer tiered rates starting at $100,000, so you’ll earn even more interest the more you invest.*

- Remember, it’s beneficial to have your interest compound in your GIC, as exponential growth can significantly increase your investment over time.

- GIC maturity is a great time to re-evaluate your investment mix. What are your financial goals, and does your investment timeline need to be adjusted (e.g. if you need to retire sooner than you initially planned)? Why did you choose to invest in a GIC, and does it still make sense with current market conditions? Is it better for you to diversify your portfolio by putting a portion of your savings into market instruments? Contact a deposit specialist to discuss your investment mix.

2.0 Choosing the GIC that's right for you

Types of GICs

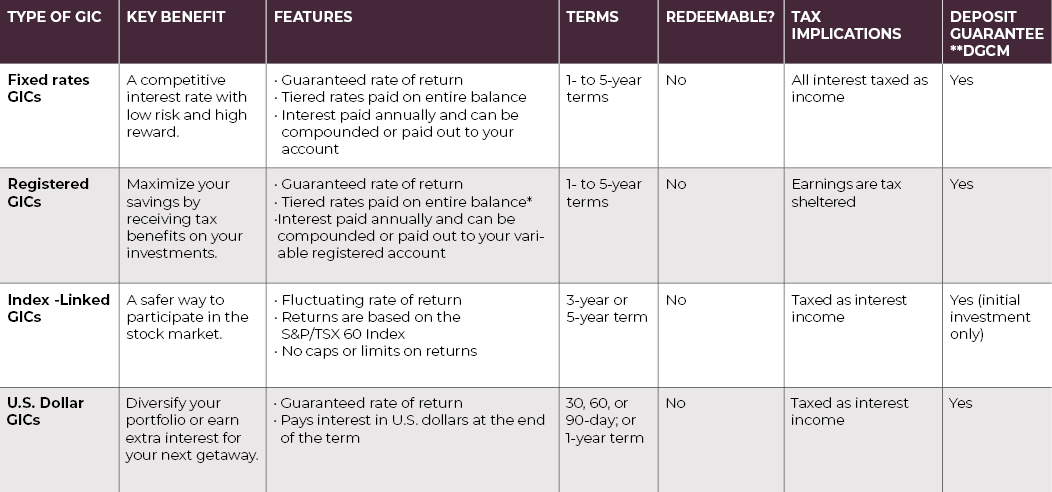

As you explore your GIC options, you’ll realize very quickly that there are many GIC choices available on the market, and each has its pros and cons. Read our overview below to determine which GIC — or combination of GICs — is right for you.FIXED-RATE GICS

Key benefit: A competitive interest rate with low risk and high reward.Fixed-rate GICs are the most common GIC products and offer a fixed interest rate for a set period. The main benefit of this account is the rates are very competitive, typically higher than a variable savings account. These

GICs are usually non-redeemable, meaning you can’t withdraw your money before the term ends. Some financial institutions will offer redeemable GICs; however, these GICs typically have shorter terms and lower rates.

Features of fixed-rate GICs at SCU

- Tiered rates start at $100,000

- Interest is paid annually and can be compounded or paid out to your account

- GICs are non-redeemable

- Deposits are guaranteed 100% by the Deposit Guarantee Corporation of Manitoba**

VARIABLE-RATE GICS (REDEEMABLE GICS)

Key benefit: A variable product with many of the benefits that come with a fixed investment.Unlike fixed-rate GICs, variable-rate GICs offer a fluctuating interest rate throughout your term and may be redeemable before the end of the term (some financial institutions have a waiting period prior to redemption). The rate is often connected to the financial institution’s variable prime rate and is typically lower than fixed-rate GICs.

Note, this product is not available at SCU.

REGISTERED GICS

Key benefit: Maximize your savings by receiving tax breaks on your investments.GICs don’t have to be a standalone product — you can hold certain types of GICs in registered investments, such as a TFSA or RRSP. It’s the best of both worlds — you’re earning a predictable return on your investment while enjoying tax breaks as you do so.

Features of registered GICs at SCU

Our registered GICs include all of the benefits of our fixed-rate GICs, plus the additional features of each registered product. Index-linked GICs and U.S. Dollar GICs are not available in registered accounts.

Explore your investment options and learn more

INDEX-LINKED GICS (MARKET-LINKED GICS)

Key benefit: A safer way to participate in the stock market.Index-Linked GICs (also known as market-linked GICs) allow you to participate in the stock market while protecting your principal investment. With an Index-Linked GIC, your principal is guaranteed, but returns vary

based on market performance (the S&P/TSX 60 Index at SCU). This means that if the stock market goes up, your GIC will increase in value. If the stock market goes down, you’ll receive your principal investment back, with no gains.

The specific features of this product may vary depending on the financial institution. It’s important to know what index your GIC is based on, as some markets have different risk levels. Also, be sure to ask about your earning potential. Some financial institutions keep a commission of your returns, or have caps on returns, while others do not. Another thing to keep in mind with Index-Linked GICs is the tax implications of this product. It’s always best to discuss this with an expert.

Features of Index-Linked GICs at SCU

- Offered in 3- or 5-year terms

- Returns are based on the performance of the S&P/TSX 60 Index

- Offers unlimited earning potential, with no caps or limits on returns

- Pays interest at the end of the term

- Index-Linked GICs are non-redeemable

- Initial deposit is guaranteed 100% by the Deposit Guarantee Corporation of Manitoba**

FOREIGN EXCHANGE GICS

Key benefit: Diversify your portfolio or earn extra interest for your next getaway.Foreign exchange GICs offer a guaranteed rate of interest in foreign currency. This product is beneficial for frequent travellers, or for investors wanting to diversify their portfolio. At SCU, we offer GICs in U.S. currency.

Features of U.S. Dollar GICs at SCU

- Choose from convenient 30, 60, 90-day; or 1-year terms with a minimum investment of $500 USD

- Pays interest in U.S. dollars at the end of the term

- U.S. Dollar GICs are non-redeemable

- Deposits are guaranteed 100% by the DepositGuarantee Corporation of Manitoba**

Choosing the GIC that's right for you: Comparing features and benefits

*Tiered rates are not available on GIC specials

**Deposit Guarantee Corporation of Manitoba . This guarantee covers all deposits including chequing and savings accounts, term deposits/GICs (including those with terms exceeding five years) registered deposits, and foreign currency deposits.

3.0 Making the most of your GICs

Deposit laddering

Deposit laddering is an investment strategy that helps you maximize returns while offering the liquidity to tap into your GIC funds on an annual basis. The concept is simple — divide your total investment dollars by five and deposit these smaller amounts into each of the one-to five-year GICs that we offer (or as many terms as you’d prefer to have). As each term matures, you can either choose to lock it in for another five years or another term of your choice. That way, you’ll have a GIC that matures every year, giving you the option to access some of the money, reinvest what you have, or even add more funds to the maturing GIC.

ADVANTAGES OF DEPOSIT LADDERING

When determining if GIC laddering is right for you, consider the following benefits:

- You’ll earn more interest in the long run. When you consider the actual interest earned year-over-year, a laddering strategy is advantageous because it earns the average rate across all five terms. Although single GIC terms may come with higher rates, laddering GICs may earn more money overall. As each GIC term matures, you can reinvest into a five-year GIC at the current rate. This offers more flexibillity to manage your funds and the potential to earn more money over time.

- Money is still accessible when you need it. No one can predict the future. Your financial circumstances and savings goals will change over time, and you may need to access some of the funds in your GIC at some point. Deposit laddering keeps the ball in your court by giving you access to one-fifth of your investments each year, without any penalties or costs.

- You’re not as affected by the ups and downs of the market. Deposit laddering minimizes the impact of rate fluctuations, but also allow you to stay current with market trends. Variable savings accounts will fluctuate, and even if you hold a single GIC, you’re limited to investing at whichever rate is offered when your investment matures. With deposit laddering, you don’t need to guess where interest rates are going. If rates go up, you will always have money coming due every year to take advantage of the rising rates. If rates go down, you benefit by having money invested for a higher rate in a longer term.

- It’s a low-risk, secured investment. GICs are low risk because they offer a locked-in rate that is solely dependent on the length of term that you’ve chosen. In addition, at SCU, all deposits are guaranteed 100% by the Deposit Guarantee Corporation of Manitoba**.

Incorporating Index Linked GICs into your laddering strategy

Index-Linked GICs (ILGIC) are great products if properly incorporated into your GIC portfolio. The purpose of laddering ILGICs into your strategy is to create the opportunity to increase the overall rate of your return in your GIC portfolio, compared to only using traditional GICs. Plus, since ILGICs are only available in 3- or 5-year terms, they can be used to replace traditional GICs for these two term lengths.

It's important to note that the return on ILGICs is paid out at maturity and like traditional GICs, the interest is 100% taxable. It's best to speak with a deposit specialist to ensure they are purchased in the proper account to avoid painful tax consequences.

GICs for every stage of life

Whatever your age or stage, GICs can be tailored to help you reach a variety of goals. Whether you're looking to save for the short-term, safely particiate in the stock market, or are looking for a consistent source of investment income, there's a GIC for that.

While there’s no one-size-fits-all approach to investing, there is a GIC for every level of investor and need. Here are some ideas of how you can maximize your GICs, based on your stage of life:

STAGE ONE: GROWING

Even if you’re in the early stages of investing, your money still has power. Compounding interest is an effective way to grow your investments while time is on your side. Plus, if you’re putting money aside in a registered product like a TFSA or RRSP, the compound interest you earn is either tax-free or tax-deferred.As an example, the graph below compares a deposit of $4,000, earning $3.0% annually. Simple interest will accrue annually based on the original principal, remaining unchanged over time. Compound interest will accrue annually, based on the original principal plus the interest earned, each year, increasing as the principal grows.

HOT TIP

You may find it helpful to eliminate temptation by locking in your money as you save for goals like a vacation, wedding, or down payment. Keep in mind it’s still a good idea to keep some funds in a variable savings account to prepare for the unexpected.

STAGE TWO: ACCUMULATING

This stage of life is all about balance. You’re starting to think more seriously about retirement, but you also have immediate financial needs. Deposit laddering can be a great way to invest while making sure you have funds for upcoming expenses, like your annual vacation or your child’s tuition.HOT TIP

A lot can change, especially at this stage of life — maybe you’re advancing your career, growing your family, or starting a business. As your financial needs change, so will your investment mix. GICs can provide a welcome stability to your portfolio on top of market investments (or an Index-Linked GIC to invest in the market). Regular meetings with a Membership Financial Relationship Advisor can help you make sure you have the right mix for your needs and risk tolerance.

STAGE THREE: MAINTAINING

As you approach or reach retirement, your focus will shift from building wealth to protecting your portfolio. GICs are a safe and predictable option at this stage of life, as you can lock in your funds at a set rate. In addition, if you are living off the interest from your GIC portfolio, you can also use deposit laddering to structure cash flow to meet your specific needs.HOT TIP

GICs are also available within an RRIF, which keeps your RRSP savings tax-sheltered beyond age 71. This means you can continue to grow your nest egg at competitive interest rates, without paying taxes as you earn.

If you’d like advice tailored to your specific needs, you can contact us by calling 1.800.728.6440, filling out a contact form or booking an appointment.

4.0 Comparing GICs with other investment options

Trying to decide which investment option will work best for your savings goals? Here are some quick comparisons between our products to help you evaluate your options.GIC vs High Interest Savings Account (HISA)

GIC

- Generally higher rates than a variable account

- Convenient 1 to 5-year terms

- Tiered rates starting at $100,000

- Can't be deposited or withdrawn at any time

- Minimum deposit of $500

- Deposits are guaranteed 100% by the Deposit Guarantee Corporation of Manitoba**

- Long-term investments

- Creating a diverse portfolio

- Saving for a large purchase

HISA

- Earn competitive interest right from dollar one, with no hidden minimum monthly balance requirements

- Tiered rates starting at $100,000

- Deposit or withdraw at any time

- Deposits are guaranteed 100% by the Deposit Guarantee Corporation of Manitoba**

- A rainy day fund

- Everyday savings

- Saving for a large puchase

GIC vs Mutual funds***

GIC

- Offers a secure and often fixed return

- Principal investment guaranteed

- No direct fees (although you have to have a savings or chequing account to collect funds upon maturity, which may have separate fees)

- Taxed at a higher rate than mutual funds (unless put into a registered account)

- Fixed-rate GICs available in all registered accounts

- Deposits are guaranteed 100% by the Deposit Guarantee Corporation of Manitoba**

- Long-term investments

- Creating a diverse portfolio

- Saving for a large purchase

MUTUAL FUNDS

- Allows you to participate in the market with a diversified portfolio based on your risk tolerance

- Mutual funds are market-based instruments that will fluctuate in value. If your investment objectives change, mutual funds may be easier to liquidate. We recommend speaking with your Advisor to ensure this investment option fits your time frame and risk tolerance

- Opportunity to work with a professional fund manager who has the responsibility to manage the assets based on a prescribed mandate

- The Management Expense Ratio helps to cover the cost of managing the fund

- Can be tax efficient depending on underlying investments

- Available in non-registered, registered, and corporate accounts

- Mutual funds are not guaranteed by the Deposit Guarantee Corporation of Manitoba**

- Investors who are looking for a professionally managed, diverse market offering

- Investors with longer time horizons where funds aren't required for short-term goals

Tying it all together

At the end of the day, you aren’t limited to just one type of investment. For example, you may choose to keep a HISA, so you have money available when you need it, GICs to stabilize your portfolio, and mutual funds for long-term savings. A well‑diversified group of investments helps smooth out the ups and downs of the market while combating inflation.The best thing you can do when you’re not sure? Talk to an SCU deposit specialist . They’ll walk you through your financial needs, review your investment performance, and help you determine how best to diversify your portfolio to meet your short-term and long-term goals.

Take the next step

Congratulations, fellow explorer! You’ve made it to the end of the guide. Now that you’ve reached this checkpoint, it’s the perfect time to take a look at your financial goals and determine your next steps. Call us at 1.800.728.6440 to speak with a deposit specialist who can help you explore the possibilities.* Tiered rates are not available on GIC specials.

**Deposit Guarantee Corporation of Manitoba . This guarantee covers all deposits including chequing and savings accounts, term deposits/GICs (including those with terms exceeding five years) registered deposits, and foreign currency deposits.

*** Mutual funds and other securities are offered through Aviso Wealth, a division of Aviso Financial Inc.